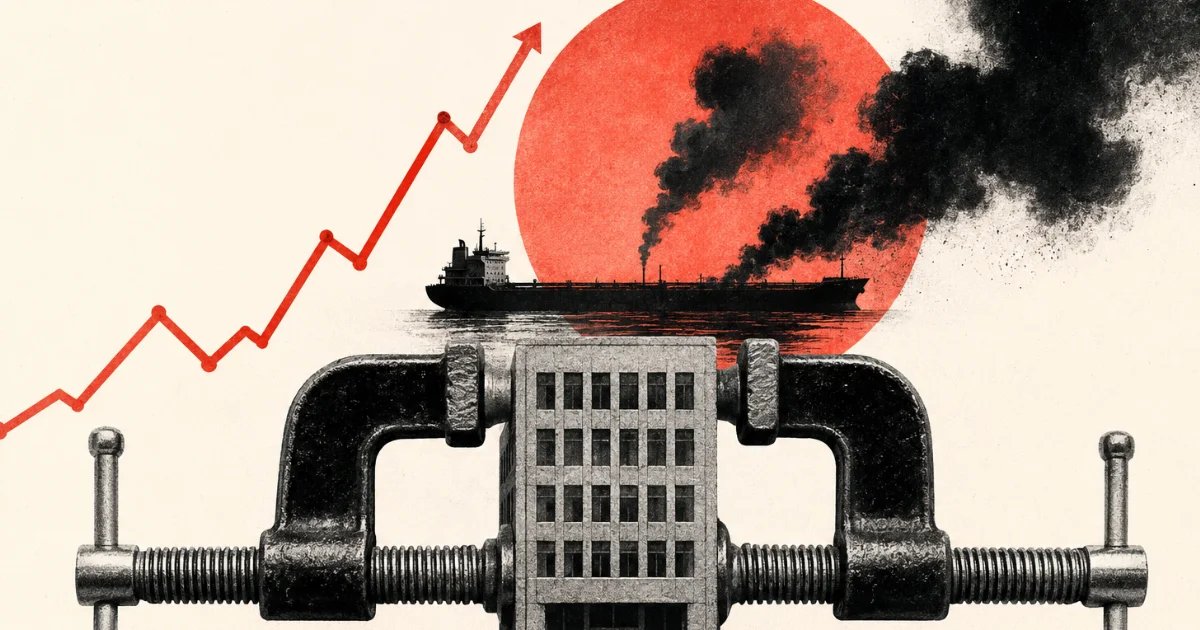

Energy Costs Are Hitting Firms First

UK businesses are being squeezed from the most basic angle: the cost of keeping the lights on. Higher energy prices ripple through almost every sector, but they land hardest on firms already working with thin margins. When power and fuel become more expensive, the effect is immediate, visible and difficult to absorb.

That pressure is not arriving in isolation. It is hitting companies that are already dealing with wage inflation, tax rises and weaker consumer demand. For many smaller firms, there is no spare capacity left to soften another jump in overheads.

The result is a business environment where even modest shocks can tip balance sheets into danger. A rise in energy bills is not just a line-item problem; it can affect pricing, staffing and investment decisions all at once.

Shipping and Supply Chains Add More Friction

The Iran conflict is also feeding through to logistics, and that matters almost as much as energy. Higher freight charges, insurance costs and transport delays all add friction to the system. Even firms that are not directly exposed to the region can still end up paying more for imported goods and components.

This is where the pressure becomes more subtle but more damaging. A business may not see a dramatic spike in a single invoice, yet the accumulation across stock, delivery and supplier contracts steadily erodes profitability. Over time, that makes working capital tighter and planning less reliable.

Supply chains hate uncertainty. When businesses cannot predict input costs or delivery schedules, they become more cautious about orders, hiring and expansion. That caution slows activity across the wider economy, not just within the firms directly affected.

Insolvency Risk Rises When Margins Are Already Thin

The real danger is not the war on its own, but the fact that it is arriving when many UK companies are already fragile. Insolvency tends to rise fastest when higher costs meet weak confidence and limited cash buffers. That combination leaves little room for error.

Once margins are squeezed, businesses often respond by delaying investment, freezing recruitment or passing costs to customers. None of those options is ideal, and each has limits. If customers are already under pressure themselves, price rises can only go so far before demand starts to weaken.

That is why insolvency numbers matter as a warning signal. They show where cost pressure has moved from being a challenge to becoming an existential problem. In practical terms, the businesses most at risk are usually those with debt, low reserves and high exposure to energy or imported inputs.

The Data Points to a Broader Business Squeeze

Surveys from business groups suggest this is not a niche problem. A large share of firms report higher energy costs, shipping disruption and supply chain stress linked to the conflict. That does not automatically mean collapse, but it does mean widespread deterioration in trading conditions.

The important point is that these pressures overlap with other domestic headwinds. Labour costs remain high, confidence is weak, and many firms are reluctant to commit to long-term investment. Add geopolitical instability into that mix and the outlook becomes more defensive than growth-oriented.

For policymakers, the message is straightforward: businesses need stability, not more surprises. For company directors, the lesson is equally blunt: cash flow discipline matters more when external shocks become harder to predict. In that environment, resilience is not a slogan; it is the difference between absorbing the hit and failing under it.

What This Means for the Months Ahead

If energy and transport costs remain elevated, more UK firms are likely to struggle. The first signs will probably appear in delayed investment, tighter hiring plans and more aggressive price rises. After that, insolvencies usually follow where balance sheets are weakest.

The broader economy may still avoid a dramatic collapse, but that is not the same as being healthy. A market can continue functioning while a growing number of firms quietly come under strain. That is exactly the kind of environment in which a cost shock becomes a wave of business failures.

What matters now is whether these pressures fade or harden into a new normal. If they do, the story will no longer be about a temporary squeeze. It will be about a sustained period in which UK businesses are forced to operate with less room for manoeuvre, less confidence and less tolerance for error.